IORP II and the top 10 considerations

IORP II is the name given to EU Directive 2016/2341. This directive is aimed at the activities and supervision of institutions for occupational retirement provisions (IORPs). It prescribes new requirements on, among others, the provision of information on pension benefit statements, the introduction of ‘key functions’, and the performance and documentation of risk management activities, while considering Environmental, Social and Governance (ESG) factors. The directive applies to all IORPs based in the EU and came into force on 13 January 2019. With regards to the approaching date of Brexit, UK IORPs must comply with the requirements set out in this directive until the UK exits the EU. The UK Department for Work and Pensions (DWP) has confirmed that it will honour this obligation.

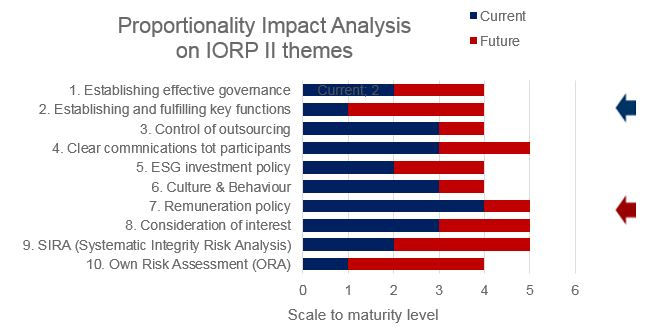

The 10 most important issues - a trigger for Internal Audit

The implementation of the IORP II directive offers a reinforcement of the governance practice, but also leads to various dilemmas. In this instance we focus on the interpretation in the Netherlands. Questions such as: ‘how to set up key functions according to the nature and complexity of the fund’ or ‘what can I expect from the outsourcing of key functions’ have yet to be answered. In the chart below you can find the 10 most important themes from IORP II (maturity level included as an example). The most obvious (and perhaps most radical) changes, and their intersection with internal audit, regarding the Dutch market will be discussed in this article.

This added value lies in aspects such as the offering of an overview and providing management insight of the most important risks, the provision of a positive impulse to the controlled operation and integrity of a pension fund, and providing more transparency and greater comfort to stakeholders (and participants) through interaction with management, the other key functions and the external auditor. Download the full article.

For more information