Egle Mockaityte

IFRS 9 introduces numerous changes (Phase 1/ classification, Phase 2/ impairment, Phase 3/ hedge accounting, disclosures) and its implementation is complex.

We chose to study the 2017 year-end financial reports of 16 European insurance and reinsurance Groups with the aim of identifying trends, progress and the impact they expect on their financial statements when first applying IFRS 9, and sources of these impacts.

We also had a look at a sample of European bank insurers to see whether they are planning to defer the application of IFRS 9 for their insurance activities.

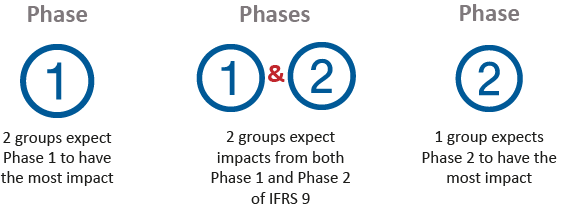

We have also analysed the expected IFRS 9 impacts by phases that (re)insurers had opted for deferral to 2021. Among the 5 groups distinguishing between the impacts of different phases* of IFRS 9, the main findings are as follows:

*Phase 1 of the standard introduced new requirements for the classification and measurement of financial instruments;

Phase 2 of the standard introduced new impairment principles;

Phase 3 of the standard introduced new rules for hedge accounting.

At the end of February 2018, all the major European banks published information on the impact of the implementation of the new standard IFRS 9. IFRS 9 introduces numerous changes (classification, impairment, hedging, etc.). Their impacts at the transition date vary widely from one bank to another. They are negative in most cases, but for some banks are virtually nil or even positive. The indicators...

Reinsurance, also known as the “ insurers’ insurance ”, plays a key role in the global market economy today. Several factors, such as the strengthening of capital requirements, the increasing level of significant NAT CAT events or the need for optimal coverage is increasing the need for reinsurance.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.