The new standard IFRS 15 on Revenue recognition for construction, civil engineering and real estate development industries

About usNews, publications and mediaOur publicationsSurveys and studies

IFRS 15 for the Real Estate Sector

Businesses in the construction, civil engineering and real estate development industries are about to face the implementation of a major standard incorporating the new principles of revenue recognition: IFRS 15.

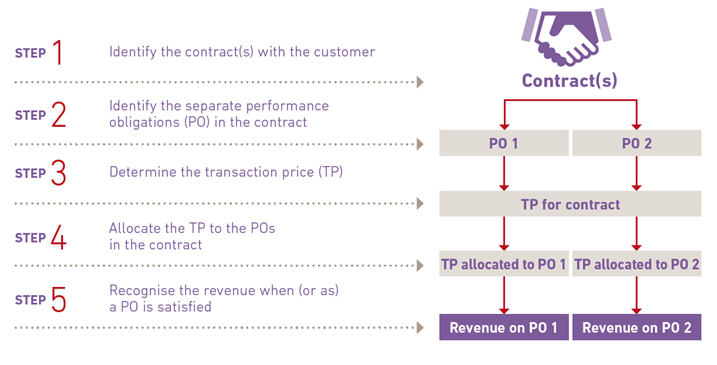

This standard relies on the concept of transfer of control to recognise revenue, rather than on risks and rewards as previously. It requires a contract to be broken down into distinct performance obligations, each with their own margin and pattern of revenue recognition.

Could IFRS 15 therefore call into question the recognition of revenue according to the stage of completion, or lead to a change in the pattern at which revenue and/or the margin is recognised?

We have analysed the 5-step recognition model set out by IFRS 15 and highlighted its implications for the real estate sector.

Find out more in our insight below.

Shahab Moreh Partner, Global Head of Real Estate - New York, United States